Futures Market: Overnight, LME copper 3M opened at $9,932.5/mt, dipped to a low of $9,927/mt during the session, then fluctuated upward to hit a high of $9,998.0/mt, and finally closed at $9,997.5/mt, up $95.5/mt or 0.96% from the previous close of $9,902.0/mt. Trading volume was 17,485 lots, and open interest reached 288,619 lots. Overnight, the SHFE copper 2505 contract opened at 81,060 yuan/mt, dipped to a low of 80,850 yuan/mt during the session, then fluctuated upward to hit a high of 81,260 yuan/mt, and finally closed at 81,230 yuan/mt, up 580 yuan/mt or 0.72% from the previous close of 80,890 yuan/mt. Trading volume was 40,412 lots, and open interest reached 242,320 lots.

[SMM Copper Morning Briefing] News: (1) According to SMM, the President of Panama announced on March 13 that he had approved the export of 120,000 mt of Cobre Panama copper concentrates. These 120,000 mt of copper concentrates will be shipped to the Onsan smelter in South Korea and three smelters in Japan, with none entering the Chinese market.

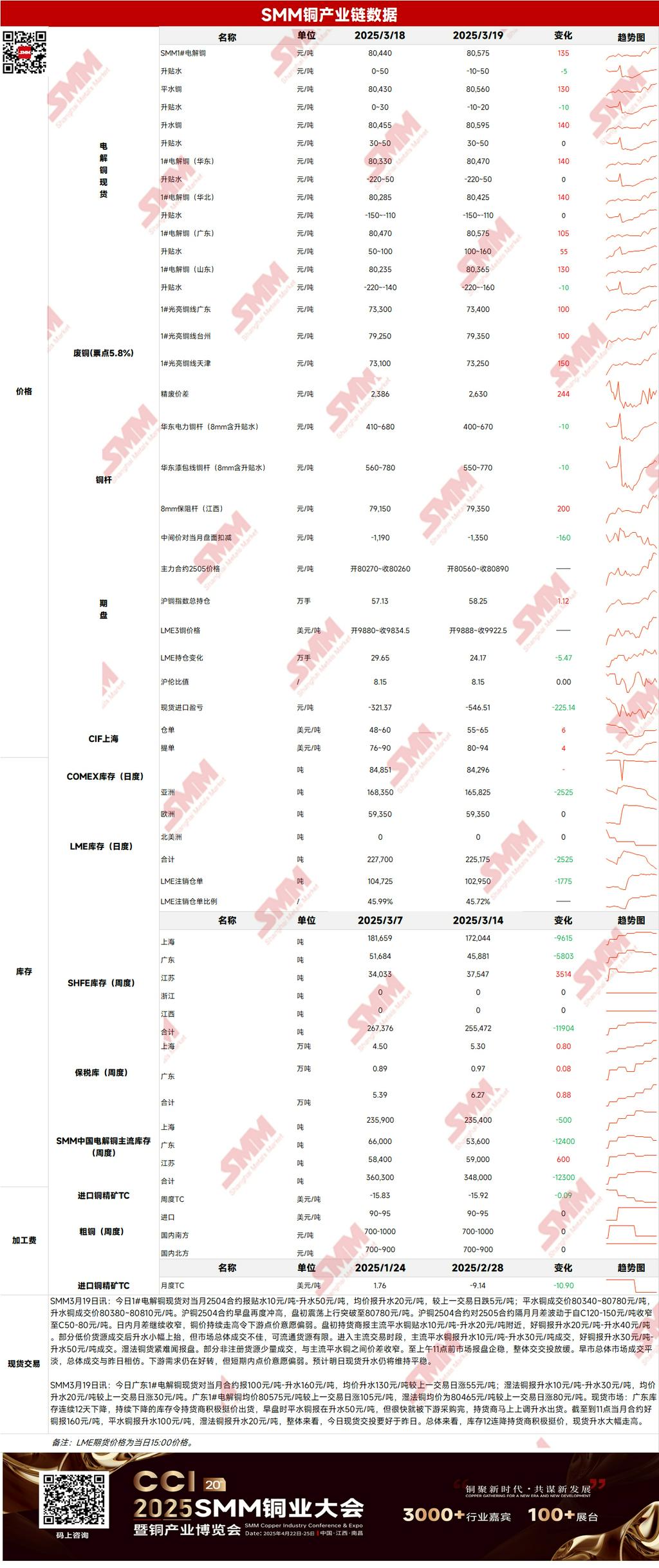

Spot Market: (1) Shanghai: On March 19, mainstream standard-quality copper spot prices against the front-month contract were quoted at a discount of 10 yuan/mt to a premium of 20 yuan/mt, while high-quality copper was quoted at a premium of 30 yuan/mt to 50 yuan/mt. Early trading saw mediocre overall market transactions, with total trading volume similar to the previous day. Downstream demand continued to improve, but short-term interest in pricing remained weak. Spot premiums are expected to remain stable tomorrow.

(2) Guangdong: On March 19, #1 copper cathode spot prices against the front-month contract were quoted at a premium of 100 yuan/mt to 160 yuan/mt, with an average premium of 130 yuan/mt, up 55 yuan/mt from the previous trading day. SX-EW copper was quoted at a premium of 10 yuan/mt to 30 yuan/mt, with an average premium of 20 yuan/mt, up 30 yuan/mt from the previous trading day. The average price of #1 copper cathode in Guangdong was 80,575 yuan/mt, up 105 yuan/mt from the previous trading day, while the average price of SX-EW copper was 80,465 yuan/mt, up 80 yuan/mt from the previous trading day. Overall, with inventories declining for the 12th consecutive day, suppliers stood firm on quotes, and spot premiums rose significantly.

(3) Imported Copper: On March 19, warrant prices ranged from $48/mt to $60/mt (QP April), with the average price up $4/mt from the previous trading day. B/L prices ranged from $76/mt to $90/mt (QP April), with the average price unchanged from the previous trading day. EQ copper (CIF B/L) was quoted at $20/mt to $30/mt (QP April), with the average price up $5/mt from the previous trading day. Quotes referenced cargoes arriving in late March and early April. Early trading saw firm market offers, with prices for registered, EQ B/L, and warrants all rising, but actual transactions remained limited.

(4) Secondary Copper: On March 19, secondary copper raw material prices rose by 200 yuan/mt MoM. Guangdong bare bright copper prices ranged from 73,300 yuan/mt to 73,500 yuan/mt, up 200 yuan/mt from the previous trading day. The price difference between primary metal and scrap was 2,630 yuan/mt, up 244 yuan/mt MoM. The price difference between primary and secondary copper rods was 1,885 yuan/mt. According to the SMM survey, the discount of secondary copper rod prices against copper futures expanded to 1,500 yuan/mt today, significantly higher than that of anode plates. As a result, many enterprises did not immediately schedule production after taking orders, with pending orders for each enterprise reaching over 1,000 mt. Additionally, the widening price difference between primary metal and scrap increased traders' pickup volume from secondary copper rod enterprises. However, high copper prices suppressed downstream consumption, leading to secondary copper rod inventories in Guangdong and Hebei exceeding normal levels.

(5) Inventory: On March 19, LME copper cathode inventories decreased by 2,525 mt to 225,175 mt. On the same day, SHFE warrant inventories decreased by 4,104 mt to 158,495 mt.

Prices: Macro side, COMEX copper prices have reached their highest level since May last year, with the premium of COMEX copper over LME copper widening to a record $1,198/mt, surpassing the previous record set on Tuesday. Driven by the price spread, copper prices continued to rise. On March 20, the US Fed kept the benchmark interest rate unchanged at 4.25%-4.50%, in line with market expectations, and stated that economic uncertainty had increased. The dot plot indicated two interest rate cuts are expected in 2025, consistent with December last year. Additionally, the Fed will begin slowing the pace of balance sheet reduction on April 1. The US dollar index jumped initially and then pulled back, partially capping copper price gains. Fundamentals side, copper prices remained above 80,000 yuan/mt, and with the destocking cycle ongoing, premiums were unlikely to decline. Overall market transactions were mediocre, except for the South China market, which remained active, while downstream purchasing interest was noticeably under pressure. In summary, with the US dollar index at low levels, COMEX copper prices continuing to rise, and technical buying support, copper prices are expected to remain firm today.

[The information provided is for reference only. This article does not constitute direct investment research advice. Clients should make prudent decisions and not substitute this for independent judgment. Any decisions made by clients are unrelated to SMM.]